Federal reserve is printing money like there is no tomorrow to aid the economy and Americans. Its balance sheet went up by more than $3T (yes big T) in a couple of months last year. 20% to 30% of all US dollars in the history were printed in less than a year in 2020 (well actually it was a couple of clicks to print money). Most Americans received the stimulus checks as part of the aid bills. I am not planning to get into details of whether or not the amount of money Fed printed was necessary in this post. I also do not discuss where the rest of the money is spent (or is going to be spent) in this post. I keep those for later posts.

When checks were issued to Americans, I looked into details of who was eligible and who was not. To my surprise I found out that the checks were given to people based on their AGI in 2019 or 2020 tax fillings. “What??? Are you serious?” were the questions passed through my mind as I was reading the details of the bills. In this post I am going to show you why AGI was a horrible number to use to decide who should or should not receive the checks. I will also show you how a family of 4 with $200,000+ gross income received $5,600 (well because they probably needed some help).

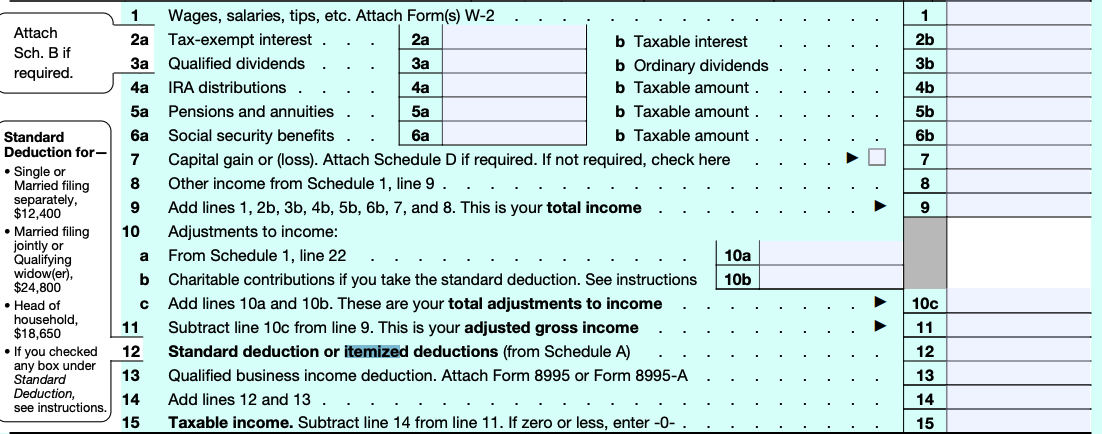

What is AGI?

Wikipedia says adjusted gross income (AGI) is an individual's total gross income minus specific deductions. It is used to calculate taxable income. To understand how it is calculated, we need to understand two things:

- Gross income

- Specific deductions

What is gross income?

Again quick Google search: your gross income is the amount of money you earn before anything is taken out for taxes or other deductions. For example, even though your monthly salary might be $3,500, you might only receive a check for $2,500. In that case, your net income would be $2,500, but your gross income is $3,500.

Gross income is pretty much all the wages, money, bonuses, capital gains, IRA distribution, etc. you receive/earn in a year. There are many different ways to earn money such as W-2, self-employed and business.

Specific deductions

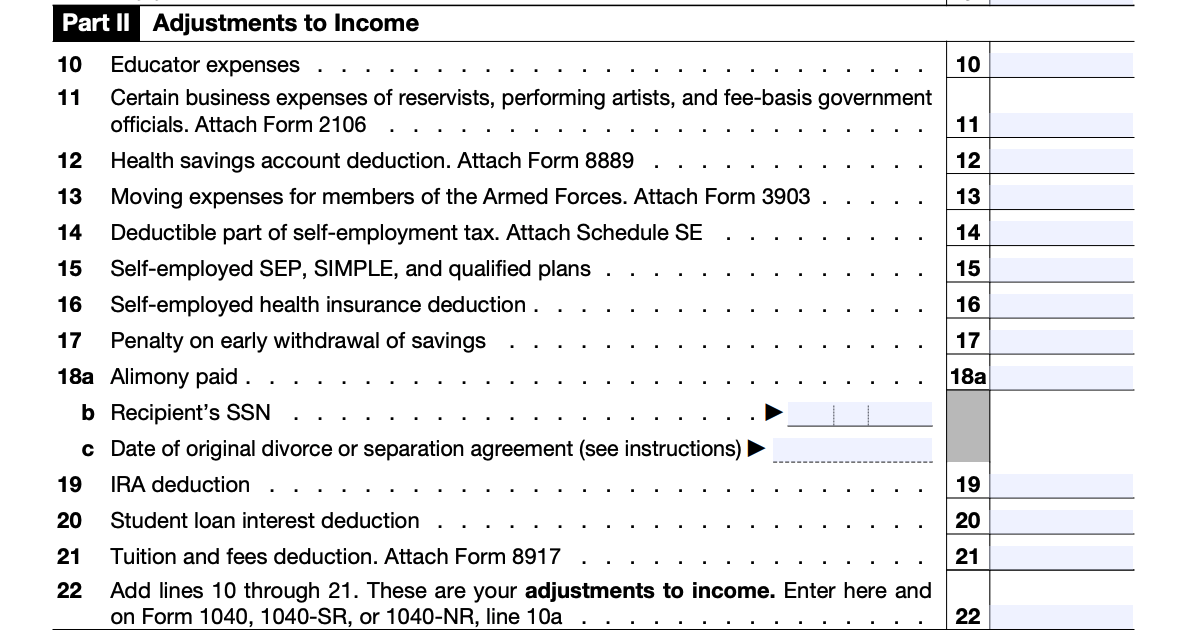

People, specially rich people, use all possible tax deductions and credits to save their wealth. Rich people have many backdoors (they also have money to hire great CPAs) to do so. I will get to techniques they use to ditch tax system in future posts. Let’s look at the possible deductions that reduce the AGI.

As it is obvious on Fig 3, there are many ways to reduce your AGI.

- Student interest rate

- IRA deduction

- Health saving account deduction

- Self-employed SEP (up to $57,000)

- Tuition

- …

For the rest of this post, I will only focus on one popular case. The case in which a couple is employed by an employer.

If you are like me, you get paid by an employer. Consider a situation in which a couple with 2 children each making $100K per year. As mentioned earlier, the upper class, upper middle class and middle class families use tax deduction and credit to fullest to minimize the amount of the tax paid to the government. Let’s assume each couple contribute to his/her own 401K and IRA.

- $19,500 per person deduction for 401k

- $6,000 per person deduction for 401k

Let’s also assume each person has a student loan that follows average student loan amount ($32,000) with average interest rate of 5.8%. Each person, then, pays about $1000 interest per year.

If we sum only these 3 adjustments, we end up with $53000 deduction. Boom! The couple is eligible for all 3 stimulus checks (AGI = $200,000 - $53,000 = $147,000) which is less than $150,000.

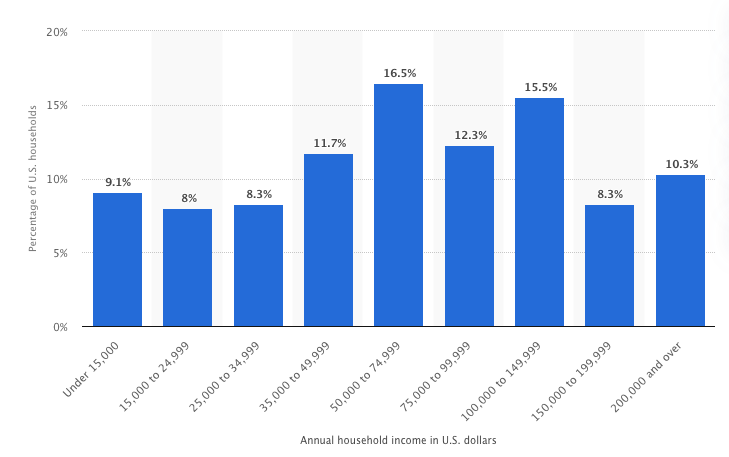

I only used a very simple case here to prove my point. Things get even worse if we include other adjustments into the equations. Things like adjustments for the health saving account ($7100 per year) or Self-employed SEP (up to $57,000 adjustment). In that case, a couple with $250,000+ gross income was even eligible to receive the checks. Now let’s look at the income distribution in the U.S to see how many households potentially received the aids.

Only about 10% of the households in the US make more than $200,000 per year. If we put all the analysis together, we can deduce that households among top 10% could potentially be eligible to receive the stimulus checks and many of them, of course, received them.

Bottom line

Ill-designed fiscal and monetary policies result in unwanted outcomes. In previous post, I showed you how following the wrong metric for inflation could benefit population asymmetrically (meaning rich becomes richer and middle class is pushed down). In this post, I showed you how looking at the wrong number benefited many who did not need any help for the most part. AGI was a wrong number to use when such policies were designed. Instead, total gross income could have been a better number to consider. I guess it is very true that ninety percent of the politicians give the other ten percent a bad reputation.

Until next time.